|

|

Enhance Knowledge

| EnhKnowTM

,

LLC

Technology Brokerage & Royalty Servicing |

|

|

|

|

| |

Business

Communications |

|

|

In Perspective: Pandemic

Company, Bankruptcy & Reorganization Viability |

|

Published: July 2, 2020 |

Original Media: This Publication |

|

Updated: None |

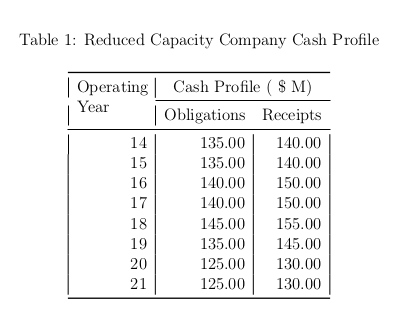

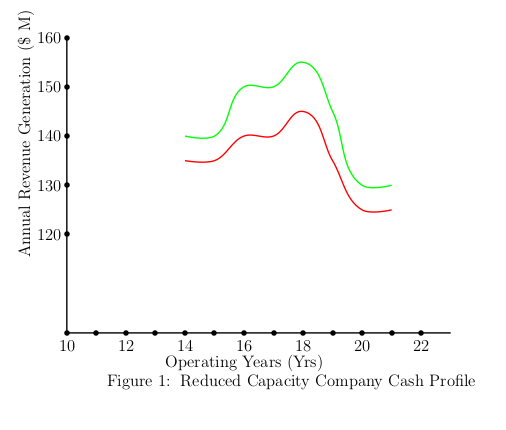

The cash profile of every pandemic

company can be set in one of two categories: Diminished [Production]

Capacity and Interrupted [Production] Capacity; and as delineated

presently, by portrayals with their cash flow profiles. The two cases

are consequences

of the demand of Social Distancing, company staffs refusing to go to work

for fear of getting infected by co-workers, of

Executive Order of Governmental Bodies for corporations to shutdown

until further notice, and of course, also from the deprivation of

skilled staff by incidental death from the infection. So, the two extreme

Pandemic Company contexts prevailing are the case of actual shutdown resulting in Interrupted

Capacity, and the other case of reduced operations resulting in

Diminished Capacity.

Obviously the Diminished Capacity Pandemic Company represents the collection of

companies still operating but engaged on only essential systems and

available only in performing proffered production. This comes about either because the

system can not be shut down or is sufficiently automated as to be

operational virtually unmanned, or by happenstance the operations have

always not entailed congregating of staff as to warrant a complete

shutdown because of the impossibility of observing Social Distancing.

Whatever the circumstance the cash profile of such company is as shown

in the Fig 1; both the Cash outflow and Cash |

|

|

inflow Profiles rapidly steeply decay to a lower equilibrium state, but not with discontinuity

in either profile. In either case the profile drops to a level reflecting

the

reduced production capacity.

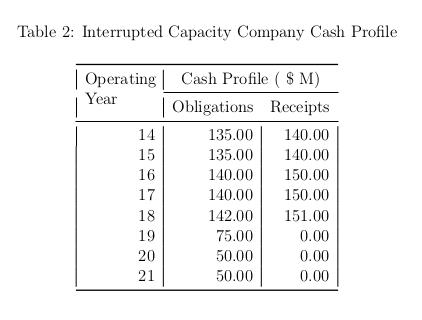

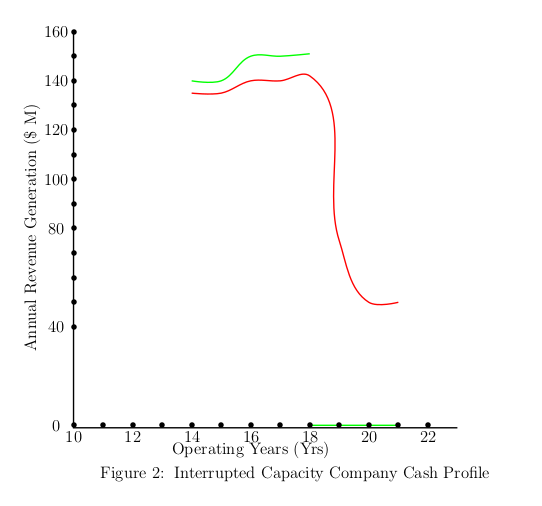

Clearly, the Interrupted Capacity Pandemic Company, as can be

readily surmised, represents the collection of companies that ceased all revenue generating operations. This comes

about most certainly from Governmental Executive Orders for corporations

of the class of non-essential operations to shutdown until further

notice. So then in this case, more specifically, the cash inflow profile

as shown in Fig 2. does not only actually fall below the cash outflow

profile but rather suffers |

|

|

|

a negative Step Jump or

Discontinuity drop and actually also becomes zero-valued. The Cash

outflow Profile, on the other hand, only drops to a new level. The drop

of the cash outflow profile is due to the shedding of variable costs

with the interruption of operations, the reduced level however is the

sum of the all non-variable costs or fixed costs of the company such as

real estate leasing, as example. Contrasting both profiles with the Cash

Profile conditions that defines Bankruptcy Company at the time of

filing for bankruptcy protection have been extensively developed and

defined in Bankruptcy, Reorganization

and Viability Analysis; the Interrupted Capacity Pandemic Company

profile qualifies as characterizing every Pandemic

Company of the category of Interrupted Capacity is technically a

Bankruptcy Company. However, the Bankruptcy Company of the class of

Interrupted Capacity Pandemic Company is specially unique with respect

to planning a reorganization, because as there does not exist the option of adjusting the

Cash outflow such as to become any lower than

the zero-value Cash inflow, and consequentially generate positive cash flow as to

enable resumption of business operations.

So then, for a pandemic Bankruptcy Company, the resumption of business

operations must be supported on the primary action of infusion of cash

of such amount as creates a Step Jump of the Cash inflow Profile to a

level above the Cash outflow Profile,

and as secondary action of establishing an upgrade context

making the Step Jump cash infusion to be self sustaining by rapid

circulation, in the

sense that the operations receive the revenue generated, in course, of

operation to support the cash inflow level of resumption as to grow from

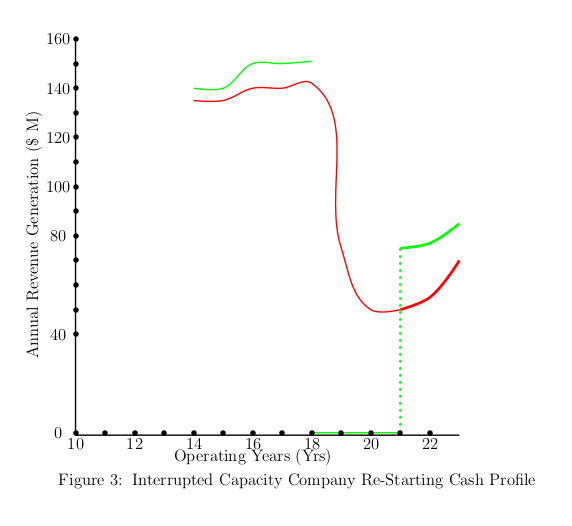

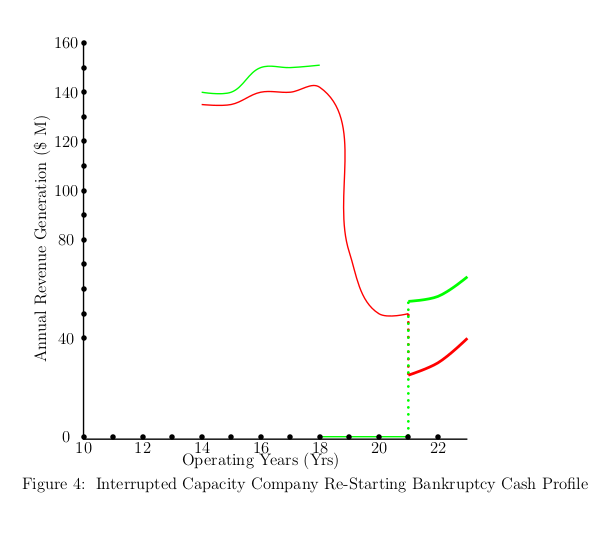

thereon. Two possible approaches to enabling the resumption of operation

are depicted in Figs 3 and 4, with both cases showing the Step Jump of

the Cash inflow Profile. Needless |

|

|

|

to state, the Cash outflow management approach differentiates the two

approaches. In Fig 3, the Cash outflow is not managed but rather left as

is at resumption of operation, while in Fig 4, the Cash outflow is

managed in a form of partial Reorganization of the bankruptcy state of

affairs. So the former does not acknowledge bankruptcy while the latter

does. Of course, which option is chosen by the Pandemic company

management likely will depend on the financial state of the company, as

also will the specifics of the implementation.

In any event, satisfying the secondary

action for resumption such that a

Pandemic Company is vested with viability from the onset is the more difficult

of the actions to be undertaken for the

Pandemic Company to viably resume operations.

The complexity of this situation is best reflected by the challenges

inherent in the construction of the

viability

analysis datasets, as shown in Corporation Viability Analytics

discussing the evaluation of business viability. Intrinsic in those

constructions of the datasets are two critical factors: The verification

of the production cost of unit product, The due diligence asserting

the inflow of revenue generated in fulfillment of sales order.

Constructing the viability datasets for a Pandemic Company entails

extensive computations -- an this is true for both the Interrupted

Capacity Pandemic Company and for the Diminished Capacity Pandemic

Company. The fact is that the unit product case is

computed through Supply Chains prevailing, and the revenue is computed

through the Buyer Chains prevailing.

As noted in other posts one potentially

surviving form of the Pandemic Company has the construct dubbed Wholistic Corporation,

which has the advantage of seller end-user products and effected

synergistic conglomerate to circumvent issues of pandemic-disrupted

Supply Chains. In essence though, that tactics for addressing the issue

of disrupted Supply Chain is a form of Reverse Vertical Integration. Inferentially then even the Reverse

Vertical Integration effects would factor

into the computation-intensive construction of the viability datasets. All these considerations,

clearly, suggests that

the required constructions of the datasets, in this context, incorporate

into the analysis the

production engineering management and designs of the company; then, of

course, the expansive repeatedly analysis of expansive designs of

Reverse Vertical Integration requires M&A Adopter

Venture Brokerage in guidance of the alternative designs towards

discovering viability datasets as input to the Viability Analytics. This

singular computational

demand to construct viability datasets of simultaneous verification of

Supply Chains and Buyer Chains to the end of restarting Interrupted Capacity

Pandemic Company embodies special requirement of

constructed strategic viability designs-set for Stability Analytics within the

Viability Analytics such as is performed with

Business Enduring Viability Analytics and which consequentially must

be adopted in performing Viability Analytics ascertaining the Pandemic

Company Viability. |

|

|

|

|

|

|

|

|